Oh, Deere — Are Investors Facing a Bumpy Ride?

Deere & Co Deep-Dive - Part III

Welcome back to — yes, already — Part III of our Deere & Co deep-dive.

If you joined us last week in Part II, you’ll recall we took a rather sunny view of the company, pretending (just for fun) that Deere had no flaws. We zoomed in on its strengths and opportunities, brushing aside the risks for another day.

For those who missed it (no hard feelings — but really, go read it; the link’s below this article), here’s the short version: Deere is a giant in its space, boasting iconic machinery, a devoted customer base, and a nicely diversified revenue mix. What’s more, it’s standing at the edge of an exciting transition — shifting from a traditional hardware business (selling “just” equipment) to a more layered software-and-services model (think precision agriculture tech, data platforms, and post-sale services).

But today, we turn the tables.

The question on the table: If you wanted to short Deere & Co, what would you focus on?

What potential risks, weaknesses, or headwinds might make you bet against the stock?

Just to be clear, I haven’t had a sudden change of heart. This is about giving risks and opportunities each their proper space, so we can walk away with a balanced, well-rounded view of the company. If you haven’t yet, I strongly recommend checking out Part II to complete the picture.

For now, though, pour yourself a fresh coffee, slip on your critical-thinking goggles, and let’s dive into the other side of the Deere & Co story.

Moat At Risk?

Assigning a clear “moat” — that protective edge that keeps competitors at bay — to any company’s strategy is always a tricky exercise. But if I had to name one for Deere & Co, I’d point to high switching costs.

Once you’re a Deere customer, you’re essentially locked in.

Why?

Because Deere says so.

Okay, that’s a little cheeky, but here’s the reality: Deere has a longstanding policy (and they’re hardly the only big player doing this) that only authorized Deere dealers can handle repairs on their equipment. Whether it’s specialized software, proprietary spare parts, or diagnostic tools, if something goes wrong with your tractor, you have to go back to an official Deere partner.

On the surface, this sounds like a solid business move. After all, it keeps service quality under control, ensures proper use of equipment, and keeps revenue flowing through official channels.

But here’s where it gets complicated.

First, there’s a legal cloud hanging over this setup. Deere was recently hit with a monopolization lawsuit, precisely because of these repair restrictions. It started in Illinois, Deere’s home state, and soon four other key states joined the case. The authorities argue that deliberately excluding independent repair shops is unfair and anti-competitive. Even if Deere ultimately dodges legal penalties, the scrutiny itself isn’t exactly good PR.

Second, and arguably more important, this policy impacts customer experience — and not always for the better.

Despite Deere’s impressive footprint — over 2,200 dealerships across the U.S. — many customers report needing to travel long distances just to reach a dealer. For farmers, where timing is everything, downtime can be devastating. A broken-down tractor during planting or harvest isn’t just an inconvenience; it can mean real financial loss. So, having a nearby, reliable service partner isn’t a luxury — it’s a necessity.

And here’s the kicker: all the exciting opportunities Deere has in shifting toward a service-based, long-term partnership model hinge on delivering that sense of reliability and support. Yet, based on many farmer reviews (and yes, I know reviews should be taken with a grain of salt), it seems some Deere customers feel that “partnership” is missing.

If customers don’t feel cared for, if they’re not confident they can get help when and where they need it, then pivoting to a service-heavy business model becomes a much steeper climb.

For me, this is a crucial point — because it cuts right into the heart of Deere’s long-term story: keeping customers loyal over time. And that’s not something we can afford to overlook.

Instability

In 2024, Deere & Co — the iconic maker of those big, green tractors rumbling across America’s farmland — trimmed its workforce from about 83,000 employees to roughly 75,850, according to Statista. Sure, that’s still a massive headcount by any standard, but it marks a cut of just over 8.5%. And let’s be honest: in corporate terms, that’s no tiny pruning — that’s a pretty hefty trim.

What’s behind the layoffs? Deere has pointed its finger at weak customer demand, essentially saying that uncertain market conditions are weighing down even this agricultural giant. It’s a reminder that no matter how mighty the company, when farmers hesitate to place orders, the factory floors get quiet.

Mexico

As if that weren’t enough, Deere also plans to shift part of its manufacturing operations to Mexico. Now, on paper, this sounds like smart business: lower labor costs and access to a growing agricultural market south of the border. Cheaper production? Expanding footprint? What’s not to like?

Well, here’s the catch — and it’s a political one. Moving jobs out of the U.S. doesn’t exactly endear you to your core customer base, especially when many of those customers are conservative-leaning American farmers. These are the folks who supported the president who, you’ll recall, proposed building a wall between the U.S. and Mexico. Not exactly the audience thrilled about U.S. companies packing up shop and heading south.

To make matters more precarious, former President Trump has already floated the idea of imposing a 200% tariff (yes, you read that right) on goods returning from Mexico into the U.S. Tariffs, for anyone newer to the investing game, are taxes placed on imported goods — and they can sharply erode the cost savings companies hoped to achieve by manufacturing abroad. So, while Deere’s move might look good on an operational spreadsheet, it risks alienating loyal customers and exposing itself to future political and economic penalties.

Commodity Prices

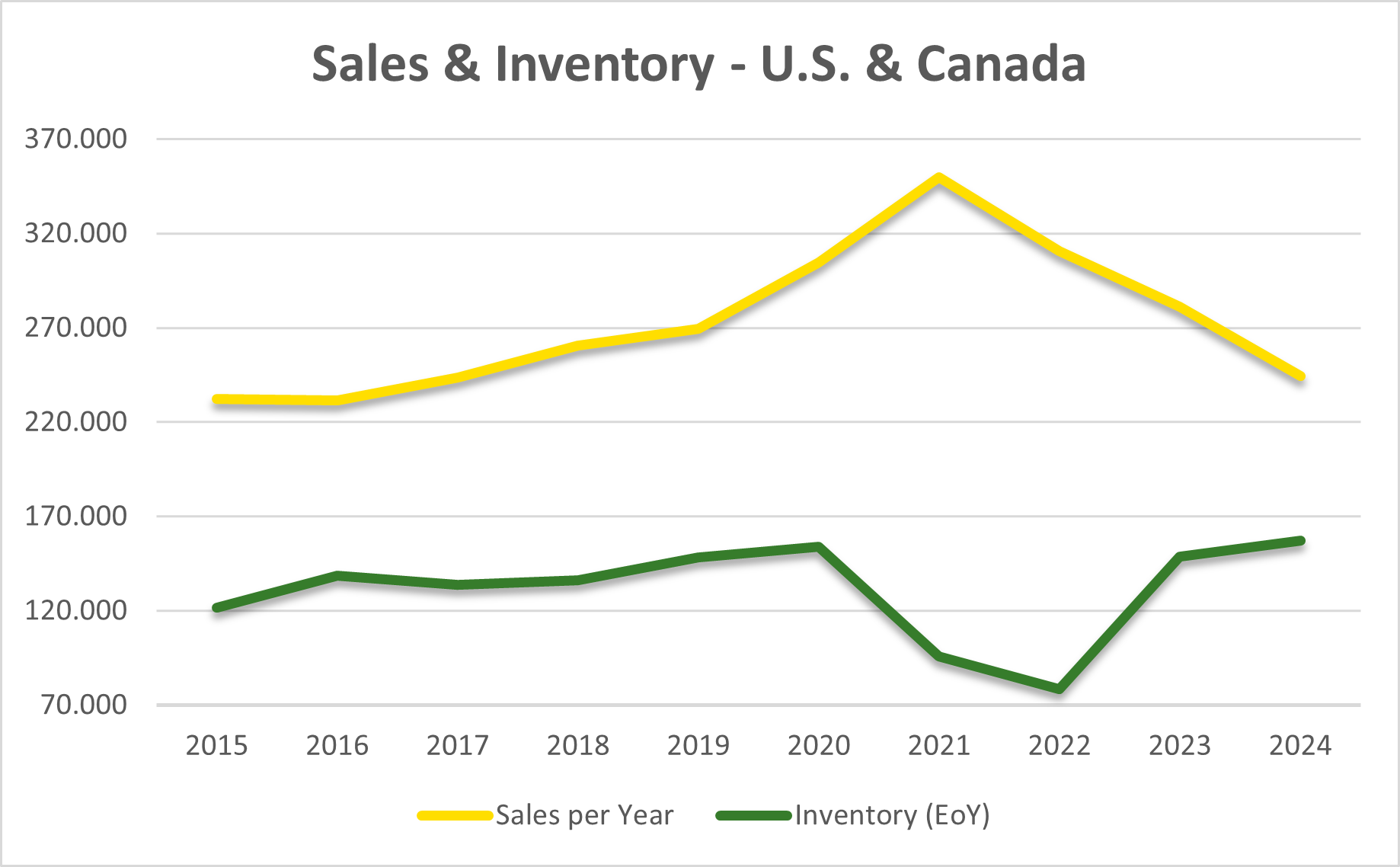

There’s also the simple but critical fact that Deere’s sales performance is closely tied to commodity prices — particularly crops like corn and soy. When farmers are getting good prices for their harvest, they’re more likely to invest in new equipment. But when commodity prices dip, so does their spending appetite, leaving Deere with fewer sales. The graphs below show this relationship clearly - Graph 1 represents the price of soy, while Graph 2 represents the sales and inventory levels of Deere:

Now, to be fair, Deere’s stock price doesn’t always move in perfect sync with commodity prices — investors price in long-term expectations, after all. But personally, I’m wary. As someone whose portfolio is already pretty exposed to cyclical sectors (industries that rise and fall with the economic tides — like automotive, for example), I’m looking to balance things out.

For me, Deere right now feels a bit too risky. Between the workforce cuts, the politically fraught Mexico shift, and the dependency on fluctuating crop prices, there are just too many moving parts. I’m after something steadier — an investment with less volatility, even if it offers slightly lower returns. Sometimes, you don’t need a roaring engine; you just want a smooth, dependable ride.

Final Remarks

So, where does all this leave us?

While Deere & Co has undeniable strengths — iconic brand, global reach, and a promising transition into precision agriculture — the risks on the horizon are hard to ignore. The company’s high switching costs, once a moat, are now under legal attack and creating friction with customers who need more flexibility and support. Workforce reductions point to underlying demand pressures, and the Mexico manufacturing shift, while operationally sensible, carries political baggage that could alienate its core U.S. customer base and expose it to hefty tariffs.

And let’s not forget the elephant in the room: Deere’s fortunes are deeply tied to the ups and downs of commodity prices. When crop prices fall, farmers pull back — and Deere’s sales can take a hit. For investors, this kind of cyclicality introduces a layer of unpredictability that’s not for the faint-hearted.

Altogether, these weaknesses and potential threats make me pause. While many investors might still see an exciting opportunity here — and fair enough, there’s a lot to admire — I personally feel the story doesn’t quite hold. For me, it’s not just about running the numbers or modeling future cash flows; it’s about believing in the narrative that underpins the business.

And right now, that narrative feels mismatched.

That’s why I won’t be valuing Deere & Co further. There’s no point in crunching valuation numbers for a company whose fundamental story doesn’t align with my own investing lens.

Sometimes, the best investment decision is the one you don’t make.

💬 What do you think? Would you short Deere & Co, or do you see long-term value here? Drop a comment below — I’d love to hear your take!

📬 Enjoyed this deep dive? Make sure to subscribe so you don’t miss future insights, breakdowns, and market stories delivered straight to you!

Please note: This article includes a disclaimer regarding investment advice.

Our Recent Posts

The Way Forward For Amazon

Today, we’ve arrived at the final part of our Qualitative research on Amazon. Normally, this is the point where I’d dig back into the numbers—running a fresh check on the balance sheet and income statement before moving forward.

The Hidden Cost In Dollar-Cost Averaging

Last week, we (and by “we,” I mostly mean my sharp co-author Milan) published a piece on why “buying the dip” isn’t always the sacred mantra it’s made out to be. There are, after all, different flavors of being contrarian — that is, going against the crowd — and each flavor has its own unique implications for how you behave in the market.

From Dirt to Dollars: How Deere & Co Is Plowing a Path to Profit

Welcome back to Part II of this agricultural adventure—strap in, because we’re trading in hay bales for horsepower. In Part I, I took a quick detour through the world of farming, asking big questions like, “What makes farmers tick?” and “How does one even begin to understand this noble, dirt-under-the-nails profession?” Now, we’re turning our spotlight …