Is Amazon Undervalued?

Amazon Deep Dive Part IV

With a slight delay (blame Aris), we've finally arrived at the final — and arguably most exciting — part of our Amazon deep dive:

The Valuation.

Today, we’re asking the big question: Is Amazon a buy? At least, according to our assumptions about how the company could grow in the years ahead.

To map that growth path, we've spent the past few weeks knee-deep in qualitative research.

In Part I of this deep dive, we laid out why we believe Amazon is one of the most high-quality companies in the world (excluding the mysterious private giants, of course).

But even for Amazon, it's not all sunshine and AWS margins. That’s why Part II was our anti-thesis — a conscious effort to challenge our (very real) bullish biases.

Having dissected both the good and the bad, we were finally ready in Part III to sketch a vision for Amazon’s future. That vision now forms the foundation for today’s valuation. So before we run the numbers, let’s quickly recap our expectations for what lies ahead.

Our Future For Amazon

Alright, before we dive into the DCF, let’s step back and frame what Amazon actually is right now.

It’s no longer just the online retail giant that dominated the internet. Today, Amazon is a vast, evolving ecosystem, quietly tilting from a model driven by low-margin scale toward one powered by high-margin leverage. AWS remains the crown jewel—still under 20% of revenue, yet pulling in over 60% of operating income. That’s what happens when you’ve got 30–35% margins working in your favor. And advertising? It’s the quiet powerhouse. Forecasted to hit $56B in 2024, growing fast, and most of that drops straight to the bottom line. Even the long-drag retail segment is starting to turn a corner. North American retail margins have edged above 6%, lifted by smarter logistics and the halo effect from ads.

Then there’s Amazon Business—the B2B platform no one seems to talk about. It's already clearing $30B and is tracking toward $65B by 2026. That’s real momentum. Real optionality.

Zoom into the segments, and the momentum holds. AWS and Ads are both primed for low double-digit growth. Retail may grind along at 5–8%, but at Amazon’s size, that’s still a big swing. The real evolution isn’t just growth—it’s the mix. More high-margin revenue changes everything about the bottom line. That’s how you shift from 2% operating margins in 2022 to something north of 10% by 2025.

But here’s the rub.

Competition is heating up from every direction—Microsoft, Google, Walmart, TikTok, MercadoLibre. Amazon’s brand power runs deep in the U.S., but abroad? It doesn’t always translate. International continues to weigh on margins.

Add to that the macro threats—rate hikes, IT belt-tightening, recession jitters—and they all hit Amazon from different angles. And then there’s Amazon itself: a company that’s never shied away from bold bets—whether it’s Kuiper, Alexa, or Prime Video—without always checking the price tag.

Bottom line: Amazon is morphing into a structurally stronger business. But from a market behavior standpoint? Investors might already be pricing that in—or, worse, overestimating it.

Which brings us here. Time to unpack the assumptions. Pressure-test the narrative. And see if Amazon’s valuation leaves any room for upside—or if the risk is hiding in plain sight.

Valuing Amazon

Anyone who read Part II of our deep dive knows: valuing Amazon is no easy task.

For one, the company’s segment disclosures are murky at best. On top of that, Amazon has quietly evolved into a mini-conglomerate — which means we’re not just valuing a retailer or a cloud provider, but an entire ecosystem spanning multiple business lines and sectors.

To build the most accurate DCF possible, we turned to our valuation Yoda (though he doesn’t know it): Professor Aswath Damodaran.

Damodaran is often called the godfather of valuation — and for good reason. The man has been helping analysts see through foggy forecasts longer than most of us have been reading earnings reports.

In February 2024, he published valuations of all the Magnificent 7 companies — and generously shared the full Excel models with the world.

That spreadsheet became our starting point. From there, we updated the inputs, reworked the assumptions, and made the model our own.

And since we’re talking assumptions — let’s quickly recap ours in the table below:

AWS and advertising now drive the profit engine, while retail and logistics quietly scale into efficiency. The result? Margins trending up from just over 10% toward 15–16% over time, with revenue growth staying solid over the next 5 to 10 years.

We expect Amazon to keep reinforcing its moat through focused investments in AI, logistics, and media. Returns on capital remain strong and capital efficiency improves as the business matures. Given the quality of the business, we apply a lower discount rate in our valuation then usual (ussually around 10%). Risks remain—but structurally, Amazon looks built for durable, profitable growth.

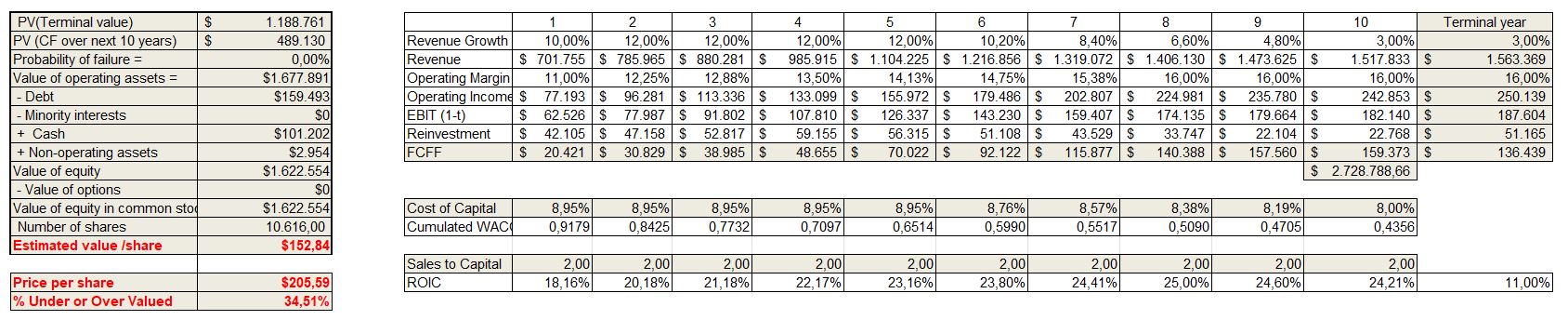

Now, if we put these assumptions into our DCF-model (of beter gezegd Damodaran zijn model). We get this result:

As you can see, our model lands on a fair share price of around $153.

That implies Amazon is roughly 35% overvalued today. Not exactly a screaming buy.

But — and there’s always a but — we think there are a few key nuances worth adding to this valuation. And for good measure, we'll also touch briefly on what Damodaran’s model concluded.

Closing Remarks

The first thing we want to say about this valuation: the fair value of Amazon is almost certainly not exactly $153 per share. That might sound contradictory, but it actually makes perfect sense.

Valuations are built on assumptions about the future — and last we checked, neither of us owns a crystal ball.

Our aim with this DCF isn’t to predict Amazon’s precise value. It’s to figure out the value we can be reasonably confident about. So while we’re not claiming Amazon is worth exactly $153, we do feel quite certain it’s worth at least that much. In other words: the margin of safety is baked in.

We’ve deliberately kept our assumptions on the conservative side. That’s how we typically roll — we’d rather risk missing an opportunity than anchor our thesis to the most optimistic version of the future. Sure, that means we might miss a few rockets. But markets are often irrational enough that even cautious investors get a chance to board.

We also chose not to capitalize Amazon’s R&D spend — which drags our valuation down further. The logic? Amazon spends billions on bold bets like Project Kuiper, with no clear path to monetization. Treating those outlays as value-accretive would be a stretch.

Damodaran did capitalize R&D in his February 2024 model, which led him to a valuation of $165 per share. And honestly? If you trust his work more than ours (and you probably should), that’s yet another signal we’ve erred on the cautious side — while still concluding Amazon looks overvalued.

So… does that mean you should dump your Amazon shares?

We wouldn’t go that far.

High-quality businesses like Amazon often trade above fair value — sometimes for years. Investors are willing to overpay for quality, because quality offers comfort. That doesn’t mean the share price is about to crash.

That said, we’re not buying at these levels either.

As much as we’d love to own Amazon, we think the price is too rich right now. After five years of investing, our worst mistakes came from betting on the rosiest scenarios. And in our view, you need the rosiest scenario to justify Amazon’s current valuation.

We hope this deep dive gave you more than just a view on Amazon — hopefully, it also gave you a glimpse into how we at DualEdge approach potential investments.

One final caveat: please take this valuation with a healthy pinch of salt. DCFs are assumption-heavy by nature, and we’re sure many of you envision a different future for Amazon.

And we’d love to hear it. Drop your take in the comments — let’s sharpen our thinking together.

Subscribe now so you get all our future Deep Dives straight into your mailbox!

Other Posts You Might Like:

[FREE] A Guide On Key Financial Metrics

![[FREE] A Guide On Key Financial Metrics](https://substackcdn.com/image/fetch/$s_!ROEx!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F3683d6c1-9bed-4f30-b7b5-dcc4982f7e20_1024x1024.png)

Warren Buffett once said that he — and Charlie Munger — never needed a computer or calculator to analyze an investment. “Too complex,” he quipped, waving off anything that couldn't be understood with simple arithmetic and sound reasoning.

The Market Punished Aris. Was It Right?

Normally, today would have been the grand finale of our Amazon deep dive series — the piece we’ve been itching to deliver because, frankly, it’s a juicy one. To everyone eagerly waiting — sorry, you’ll have to hang tight until next Sunday.

Oh, Deere — Are Investors Facing a Bumpy Ride?

Welcome back to — yes, already — Part III of our Deere & Co deep-dive.

Yes.

Valuing Amazon is an extremely challenging exercise, mostly because of their high reinvestment. Who are we to make a DCF model in which we assume Amazon will stop reinvesting the majority of cash flows over the next 10 years?

Moreover, a 10-year model is extremely conservative in my opinion: because the company has never optimized for returns, a 10-year period of excess returns seems too short, which means you're missing a lot of value in your model.

Just my thoughts