Givaudan: Smells Like a Moat

It’s been a while since we dissected a business.

The last one? Amazon. A beast in almost everything it touches — except valuation. We passed on it. Too expensive. (Though don’t worry, that full report is coming soon for premium subscribers. If you’re an Amazon shareholder, it might be time to consider the best option out there — yes, we mean going premium.)

Same story with Aris. Promising business, priced like it already solved water scarcity.

We’re seeing a pattern here. Call it the Overvaluation Era™. And it’s making us slightly uncomfortable.

Sam from Valuing Dutchman nailed it in this piece:

But not all corners of the market are equally inflated. Luckily, our friend Ozeco steered us toward one that’s been struggling quietly for years: the ingredients sector.

We did a full deep dive on the space. And the conclusion?

We may have struck gold.

🧠 Side note: If you haven’t read our full sector report with Ozeco, do that first — trust us, it’s worth your time.

After publishing that, we each took on some of the companies from the sector. Ozeco is diving into DSM-Firmenich this week.

Last week, I compared the five largest and most interesting names in the industry. After filtering out IFF and DSM-Firmenich, we were left with three prime candidates:

Givaudan, Symrise, and Novonesis.

And because we’re not dictators (and definitely not because I couldn’t decide), we let you choose via poll.

The result? Clear as day. Givaudan took the win.

Which tells me something important: you, dear reader, have taste. The kind that favors quality over hype. (Also… you picked the “boring” option. Respect.)

Now that the crowd has spoken, we can get started.

Today’s post is the groundwork. We’ll explain who Givaudan is, what they do, and how they do it — so that in the next parts, we can go deep on their economics, edge, and valuation.

🧬 Meeting Givaudan

To properly introduce Givaudan, allow me to summon my inner Walter Isaacson. (Don’t worry, he’s only staying for two paragraphs.)

Givaudan was founded in 1895 in France as a perfume house. A few years later, it moved to Geneva. Mid-20th century, it expanded into flavorings. In 1963, it was acquired by Roche, which also bought rival Roure. The two were eventually merged into Givaudan-Roure.

Then in 2000, Roche spun off Givaudan as a standalone company on the Zurich stock exchange. Since then, the company has grown through a combination of organic expansion and carefully selected acquisitions.

A major turning point came in 2007 with the acquisition of Quest International, making Givaudan the undisputed global leader in both fragrance and flavor. And the acquisition engine didn’t stop there. Since 2014, Givaudan has bought over 20 companies — including:

Naturex (natural extracts)

Parts of AMSilk (cosmetic ingredients)

Albert Vieille (essential oils)

Today, Givaudan is the #1 player in the global Flavours & Fragrances (F&F) space — ahead of DSM-Firmenich, IFF, and Symrise. (You may remember those names from… everywhere else we’ve written lately.)

What Does Givaudan Actually Do?

Givaudan S.A. is the world’s largest producer of fragrance, flavor, and cosmetic active ingredients. They develop custom sensory experiences used in:

Food and beverages

Household care (detergents, cleaners)

Personal care (shampoos, deodorants)

Fine fragrances

And more.

These aren’t off-the-shelf ingredients. Givaudan works hand-in-hand with clients to create custom, confidential, and often proprietary formulations. It’s all very hush-hush — which is part of the moat.

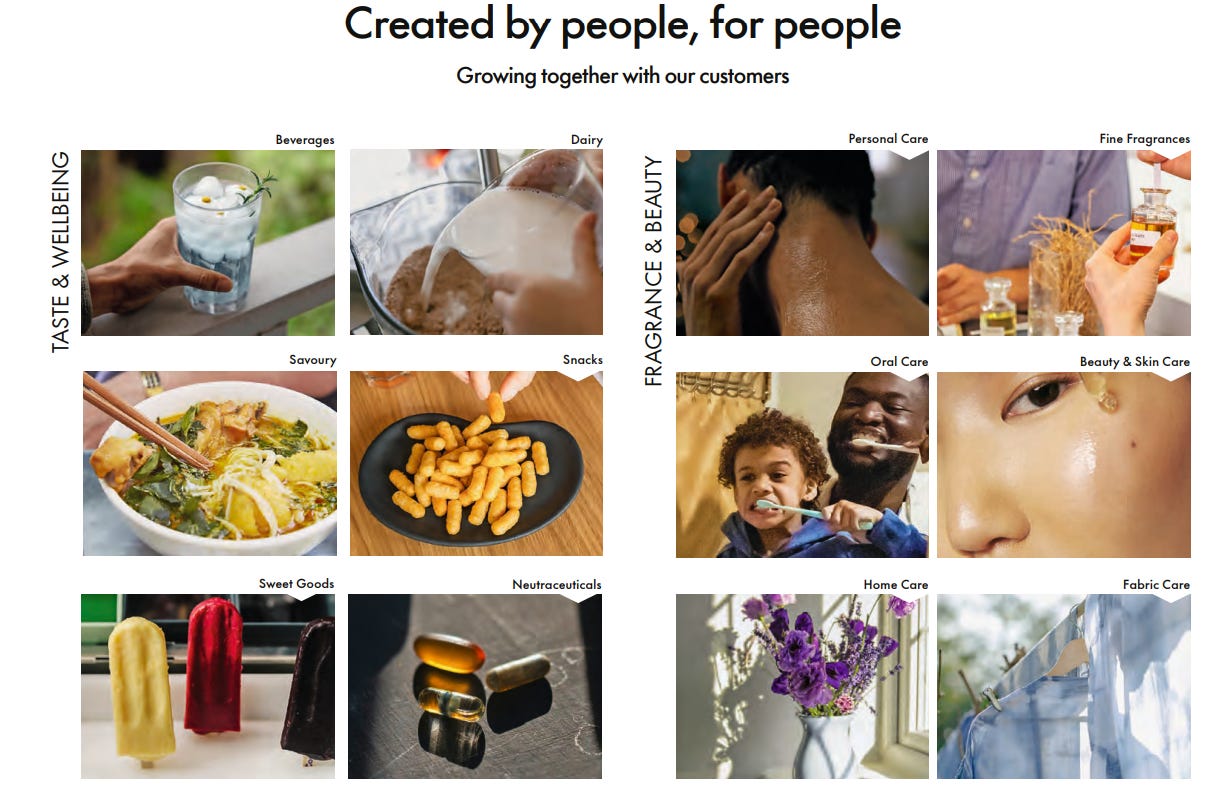

Two Main Divisions:

1. Taste & Wellbeing (52% of revenue)

Includes flavorings and food ingredients — from savory to dairy to confectionery and beverages.

2. Fragrance & Beauty (48% of revenue)

Focused on scents for perfumes, household and personal care, plus active ingredients for cosmetics and skincare.

They operate in 163 global locations, with 78 production sites and dozens of creative development centers — all optimized to tailor flavors and scents to regional preferences.

Who Buys from Givaudan?

Everyone.

Their customer list includes the who's who of the global consumer goods world:

Nestlé

PepsiCo

Danone

Unilever

Procter & Gamble

L’Oréal

Estée Lauder

Plus thousands of smaller or regional players — in fact, over 50% of revenue comes from non-multinationals. That diversity gives Givaudan solid resilience.

Revenue split by geography is also balanced:

39% from EMEA

25% Asia-Pacific

24% North America

12% Latin America

So about 46% of revenue comes from high-growth markets — the rest from mature economies. That’s a built-in hedge against regional volatility.

How Givaudan Actually Works

So how does Givaudan actually make money?

It starts and ends with innovation and R&D. They spend around 7.5% of sales (CHF 519M in 2023) on research. They hold 5,000+ active patents. The business is built around proprietary molecules, high technical knowledge, and tight client relationships.

Their global creation centers are staffed with perfumers, flavorists, and scientists who co-develop products with clients — from concept to formula. Often, these are co-created before the end product even exists.

And here’s the kicker: Givaudan holds many captive ingredients — molecules only used in their products. That gives them edge, pricing power, and sticky client relationships.

In flavor, they’ve built portfolios like TasteSolutions — helping brands reduce salt, sugar, or fat without losing flavor.

In fragrance, they offer custom molecules to give perfumes their unique identity.

And the collaboration runs deep. Givaudan often operates as a true partner, not just a supplier.

That process starts early. Very early.

As in: long before there’s even a product, Givaudan’s experts — perfumers, flavorists, sensory scientists — are already working hand-in-hand with the client’s R&D team. Whether it’s a soda brand developing a new zero-sugar variant, or a beauty company chasing the next bestseller scent, Givaudan is there at the inception.

Together, they co-create a unique taste or scent that aligns perfectly with the desired product experience and brand identity. It’s not plug-and-play — it’s bespoke. And almost always confidential.

And Givaudan doesn’t stop at delivering molecules. They offer a whole suite of services that further embed them into the client’s innovation process:

Consumer insights – What do people actually want to taste or smell? Givaudan runs studies to find out.

Application support – How does this scent behave in a detergent? Will this biscuit still taste good after baking? They test it.

Regulatory advice – Is this flavor legal in the US, EU, and China? Givaudan knows.

This depth of collaboration creates a powerful moat. The formulations are made for one customer and one customer only — and they’re often protected by confidentiality or even technical lock-in. Switching suppliers isn’t just annoying. It’s a potential product disaster.

And that’s the beauty of the model: once a Givaudan molecule makes it into a finished product, it usually stays there. For years. Sometimes decades. The upfront investment pays off in recurring, high-margin revenue that’s incredibly sticky.

Not because of contracts. But because of co-creation, trust, and a shared pipeline.

So yes — Givaudan sells flavors and fragrances.

But what they really sell is embedded expertise, defensibility, and creative IP.

Innovation: The Real Growth Engine

Their entire commercial flywheel — from first client contact to long-term revenue — is built on the ability to co-create cutting-edge tastes, scents, and sensory experiences that no one else can replicate. That’s why they invest ~7.5% of revenue into R&D annually and hold over 5,000 active patents.

And that effort pays off.

Givaudan launches hundreds of new products a year. A large portion of their revenue comes from stuff developed in just the past 5 years. That’s a key KPI in this space — it shows they’re keeping up with shifting consumer trends like sugar reduction, clean label, or “natural” everything.

Recent launches include:

Bloomful Splash – tech to measure fragrance bloom in diluted products (e.g. softeners, reed diffusers).

Amaize® Orange Red – a natural color/flavor from purple corn, replacing synthetic red dyes.

TasteCollections – Fire – a smoky new ingredient line co-developed by chefs and perfumers.

What’s cool is the cross-pollination — their teams don’t just stay in their lanes. Perfume and flavor experts work together. That’s how you end up with ideas like fire-inspired flavor notes in both BBQ chips and cologne.

This innovation engine is sustained not just by tech, but by culture. Givaudan has its own perfumers school (since 1946). Teams are cross-functional. Creativity is institutionalized. Chefs collaborate with chemists. Flavorists brainstorm with cosmetic scientists. The result? Constant evolution — and defensible uniqueness.

But while innovation is the core driver, it’s not the only one.

Scaling Scent: One Molecule, One Acquisition at a Time

Innovation may be the engine — but it’s not the whole car.

Givaudan grows in two main ways: by deepening relationships through new product development, and by expanding its platform through smart, selective acquisitions.

Let’s start with the first.

The company targets 4–5% organic growth annually. But in practice? It’s doing better. Between 2021 and 2024, average revenue growth clocked in at ~7.2% a year. That’s driven by steady volume gains (new wins, new launches) and something even more telling: pricing power. When your flavor molecule is the secret behind someone’s bestselling soda or face cream, you don’t need to discount.

And then there’s M&A. This isn’t a roll-up story or a land-grab. Givaudan doesn’t chase big headlines — it builds quietly, piece by piece. Over the past decade, it’s acquired dozens of niche players that expand its capabilities in natural extracts, active cosmetics, and specialty ingredients. Naturex was a major one. So were Induchem and Soliance. These aren’t trophy deals. They’re strategic add-ons — small companies with unique IP, folded into a bigger machine.

But here’s what Givaudan does differently: it integrates carefully, and it doesn’t suffocate what it buys. Integration spending runs around 3–4% of sales, but many of the acquired companies are left to operate semi-independently. They keep their own culture and edge — but benefit from Givaudan’s scale, global reach, and deep customer access.

The result? A model that compounds.

Innovation fuels organic growth. Acquisitions open new doors. And together, they reinforce a business that’s defensible, diversified, and built to last.

This isn’t growth at any cost. It’s growth with taste. Literally.

CLOSING REMARKS

Givaudan is the world’s largest — and arguably most essential — supplier of flavors, fragrances, and cosmetic actives. From your soda to your shampoo, there’s a good chance they’ve had a (literal) hand in how it tastes or smells.

But what makes them truly stand out is how they operate: deep co-creation with clients, relentless innovation, sticky customer relationships, and a growth strategy that blends organic development with targeted acquisitions. It’s a business that hides in plain sight — highly technical, deeply embedded, and quietly compounding.

Next week, we go from introduction to interrogation.

We’ll break down Givaudan’s true strengths, the risks that don’t show up in a scent strip, and whether this quality business is priced like a bargain… or a luxury perfume.

🔍 Stay tuned — and if you’ve got questions or angles you want us to dig into, hit us in the comments.

🔔 Don’t miss Part 2.

Subscribe now to get the full deep dive, including our analysis, valuation framework, and whether we think Givaudan deserves a spot in your portfolio — or just in your bathroom.

Please note: This article includes a disclaimer regarding investment advice.

Our Recent Posts

Who Deserves the Deep Dive? You Tell Us

Last week, together with Ozeco, we dove into the world of ingredient companies. Yes, I know — that sounds painfully boring. But hear me out.